UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 000-27436

TITAN PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 94-3171940 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer identification number) | |

| 400 Oyster Point Blvd., Suite 505, South San Francisco, California |

94080 | |

| (Address of principal executive offices) | (Zip code) | |

Registrant’s telephone number, including area code: (650) 244-4990

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $.001 par value | The American Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition or “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer |

¨ | Accelerated filer | x | |||

| Non-accelerated filer |

¨ | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the 57,982,680 shares of voting and non-voting common equity held by non-affiliates of the registrant based on the closing price on June 30, 2011 was $105.5 million.

As of March 9, 2012, 59,386,542 shares of common stock, $.001 par value, of the registrant were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

NONE

PART I

NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in this Annual Report on Form 10-K or in the documents incorporated by reference herein may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Reference is made in particular to the description of our plans and objectives for future operations, assumptions underlying such plans and objectives and other forward-looking terminology such as “may,” “expects,” “believes,” “anticipates,” “intends,” “expects,” “projects,” or similar terms, variations of such terms or the negative of such terms. Forward-looking statements are based on management’s current expectations. Actual results could differ materially from those currently anticipated due to a number of factors, including but not limited to, uncertainties relating to financing and strategic agreements and relationships; difficulties or delays in the regulatory approval process; uncertainties relating to sales, marketing and distribution of our drug candidates that may be successfully developed and approved for commercialization; adverse side effects or inadequate therapeutic efficacy of our drug candidates that could slow or prevent product development or commercialization; dependence on third party suppliers; the uncertainty of protection for our patents and other intellectual property or trade secrets; and competition.

We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations or any changes in events, conditions or circumstances on which any such statement is based.

References herein to “we,” “us,” “Titan,” and “our company” refer to Titan Pharmaceuticals, Inc. [and its subsidiaries] unless the context otherwise requires.

Probuphine™ and ProNeura™ are trademarks of our company. This Annual Report on Form 10-K also includes trade names and trademarks of companies other than Titan.

| Item 1. | Business |

Overview

Our principal asset is Probuphine™, the first slow release implant formulation of buprenorphine, designed to maintain a stable, round the clock blood level of the medicine in patients for six months following a single treatment. Daily treatment of opioid dependence with sublingual buprenorphine formulations is already a $1+ billion market in the U.S., and a transdermal formulation for the treatment of chronic pain entered the U.S. market in 2011. Probuphine is being developed for the treatment of opioid dependence with the potential to enhance patient compliance to medication, and limit diversion and accidental use of the daily dosed formulations. In October 2011, we had a Pre-New Drug Application meeting with the U.S. Food and Drug Administration (the “FDA”) that provided clear guidance on the requirements for submitting a New Drug Application (“NDA”). The clinical development program is now complete and preparation of the NDA is in process. At the request of the FDA, we are conducting additional analytical testing of the ethylene vinyl acetate (an inactive co-polymer in Probuphine) and the final product, Probuphine, in order to complete full characterization and establish ‘in-use’ stability. We have also commenced a program with our contract manufacturer to scale-up the manufacturing process for commercial production. We expect to complete these steps and be in a position to submit the NDA in the third quarter of 2012. Our goal is to enter into one or more partnerships with capable pharmaceutical companies to commercialize Probuphine in the U.S. and foreign markets, as well as to potentially develop the product for the treatment of chronic pain.

Probuphine is the first product to utilize ProNeura™, our novel, proprietary, long-term drug delivery technology. Our ProNeura technology has the potential to be used in developing products for the treatment of other chronic conditions, such as Parkinson’s disease, where maintaining stable, round the clock blood levels of a drug can benefit the patient and improve medical outcomes.

2

Under a sublicense agreement with Novartis Pharma AG (“Novartis”), we are entitled to royalty revenue of 8-10% of net sales of Fanapt® (iloperidone), an atypical antipsychotic compound being marketed in the U.S. by Novartis for the treatment of schizophrenia, based on a licensed U.S. patent that expires in April 2017 (inclusive of a six month pediatric extension). We have entered into several agreements with Deerfield Management (“Deerfield), a healthcare investment fund, which entitle Deerfield to most of the future royalty revenues related to Fanapt in exchange for cash and debt considerations, the proceeds from which we have been using to advance the development of Probuphine and for general corporate purposes. We have retained a portion of the royalty revenue from the net sales of Fanapt in excess of specified annual threshold levels; however, based on sales levels to date, it is unlikely that we will receive any revenue from Fanapt in the next several years, if ever.

We operate in only one business segment, the development of pharmaceutical products.

Our Products

Probuphine

We are developing Probuphine for the treatment of opioid dependence. Probuphine is the first product specifically designed for the long-term treatment of opioid dependence and it utilizes ProNeura, our novel, proprietary, long-term drug delivery technology. (see “Continuous Drug Delivery Technology” below). Probuphine is designed to maintain a stable, round the clock blood level of the drug buprenorphine, an approved agent for the treatment of opioid dependence. If approved, Probuphine is expected to provide six months of medication following a single treatment. Probuphine has been shown to be effective with an acceptable safety profile in the following clinical studies:

| • | Two six-month, double-blind, placebo-controlled safety and efficacy trials; one of which included an open label, active control (Suboxone). In both studies, Probuphine demonstrated superiority to placebo implants, and in the second study, established non-inferiority in comparison to Suboxone. |

| • | Two six-month, open-label re-treatment safety trials; and |

| • | A pharmacokinetic (relative bioavailability) safety study. |

The goal of any therapy for an addictive disorder is to reduce the use of the substance over time and to engage the patient in treatment long enough for therapeutic gains to be consolidated. In a clinical study, the effectiveness of a treatment for opioid dependence is primarily evaluated by testing a patient’s urine samples for the presence of illicit opioids over the treatment period. In both placebo-controlled Phase 3 studies of Probuphine, every participant was required to provide urine samples three times a week, essentially on alternate days. Any missed sample was considered a positive result (i.e. urine testing positive for illicit opioid). In these studies, the primary effectiveness of the treatment with Probuphine (i.e. the primary endpoint) was established by comparing the negative urine results (i.e. urine testing negative for illicit opioid) between the Probuphine and placebo arms using a statistical technique, specifically ‘the cumulative distribution function of negative urines’, which basically performs a comparative analysis on the relative proportions of negative urines between treatment groups over the time period of treatment. The patients in the Probuphine arm showed clinically meaningful and a statistically significant difference in the negative urines as compared to the placebo arm in both studies, i.e. the Probuphine patients had statistically more negative results than the placebo arm, demonstrating that the treatment with Probuphine was successful in reducing their usage of illicit opioids as compared to the treatment with placebo. These favorable results for Probuphine were also confirmed by a significant difference over the placebo arm in other secondary measures such as retention in treatment, withdrawal symptoms and craving for opioids, all of which are monitored by clinicians to see if a treatment is providing clinically meaningful benefit to the patients.

Results for the first double-blind, placebo-controlled safety and efficacy study have been published in the Journal of the American Medical Association (JAMA, October 2010).

3

Patients who completed the controlled studies were eligible for enrollment in the six-month re-treatment studies, which provided data on up to one full year of treatment. The pharmacokinetic safety study has provided important data on the level of buprenorphine in the blood during the treatment period and gives a good profile of the safety of Probuphine. Data from all of these studies was presented at the International Society of Addiction Medicine Annual Meeting in November 2008 and September 2011, the American Society of Addiction Medicine Annual Meeting in May 2009 and American Society of Addiction Medicine Education Forum in October 2011, and the American College of Neuropharmacology in November 2009.

These studies are part of a registration directed program intended to obtain marketing approval of Probuphine for the treatment of opioid dependence in the U.S. and in Europe. We met with the FDA in October 2011 for a pre-NDA meeting and reviewed the clinical development program as well as the chemistry, manufacturing and controls (“CMC”) aspects of the NDA. Based on this interaction we believe we do not need to conduct any additional clinical studies prior to submitting the NDA and we have commenced the final activities in the CMC area that are necessary to obtain the remaining information while also beginning the preparation of the NDA, which we hope to submit in the third quarter of 2012.

Continuous Drug Delivery Technology

Our continuous drug delivery system consists of a small, solid rod made from a mixture of ethylene-vinyl acetate (“EVA”) and a drug substance. The resulting product is a solid matrix that is placed subcutaneously, normally in the upper arm in a simple office procedure, and is removed in a similar manner at the end of the treatment period. The drug substance is released slowly, at continuous levels, through the process of dissolution. This results in a constant rate of release similar to intravenous administration. We believe that such long-term, linear release characteristics are desirable by avoiding peak and trough level dosing that poses problems for many Central Nervous System (“CNS”) and other therapeutic agents.

Our continuous drug delivery technology was developed to address the need for a simple, practical method to achieve continuous long-term drug delivery, and potentially can provide controlled drug release on an outpatient basis over extended periods of up to 6-12 months. In addition to Probuphine, which is our first product in clinical testing to utilize our proprietary continuous drug delivery technology, we continue to seek opportunities to develop this drug delivery technology for other potential treatment applications in which conventional treatment is limited by variability in blood drug levels and poor patient compliance (e.g. treatment of Parkinson disease with dopamine agonists). Titan was awarded a $0.5 million SBIR grant in August 2010 to conduct non-clinical studies with long-term delivery of dopamine agonists and this data is expected to be available in the second quarter of 2012.

Fanapt® (iloperidone)

Fanapt (iloperidone) is an atypical antipsychotic approved by the FDA for the treatment of schizophrenia currently being marketed by Novartis in the U.S. Under a sublicense agreement with Novartis, we are entitled to a royalty of 8-10% of net sales, based on a U.S. patent that we licensed from Sanofi-Aventis. The U.S. patent expires in April 2017 (including a six-month pediatric extension). Vanda Pharmaceuticals, Inc. (“Vanda”) owns the development and commercialization rights to the oral and depot formulations of this product for the rest of the world. However, because patent coverage on the compound has now expired in the significant markets outside of the U.S. and no patent term extensions are possible since the product was not approved in these countries prior to patent expiration, we do not expect any royalties on any future sales in such markets.

We have entered into several agreements with Deerfield, which entitle Deerfield to most of the future royalty revenues related to Fanapt in exchange for cash and debt considerations, the proceeds of which have been, and are continuing to be, used to advance the development of Probuphine and for general corporate purposes. We have retained a portion of the royalty revenue from net sales of Fanapt in excess of specified annual threshold levels; however, based on sales levels to date, it is unlikely that we will receive any revenue from Fanapt in the next several years, if ever. We do not incur any ongoing expenses associated with this product.

4

License Agreements

We are a party to several agreements with companies and universities for the performance of research and development activities and for the acquisition of licenses relating to such activities. Expenses under these agreements totaled approximately $36,000, $61,000 and $86,000 in the years ended December 31, 2011, 2010 and 2009, respectively.

In January 1997, we acquired an exclusive worldwide license under U.S. and foreign patents and patent applications relating to the use of iloperidone for the treatment of psychiatric and psychotic disorders and analgesia from Sanofi-Aventis SA (“Sanofi-Aventis”) (formerly Hoechst Marion Roussel, Inc.). The Sanofi-Aventis agreement provides for the payment of royalties on future net sales and requires us to satisfy certain other terms and conditions, specifically continued diligent product development and commercialization efforts standard for these types of agreements, in order to retain our rights, all of which have been met to date.

In November 1997, we granted a worldwide sublicense, exclusive of Japan, to Novartis under which Novartis continued, at its expense, all further development of iloperidone. In April 2001, that sublicense was extended to include Japan. Under this agreement, Novartis agreed to pay Titan a royalty on future net sales of the product equal to 8% of annual worldwide net sales up to $200 million and 10% of annual worldwide net sales above $200 million, in addition to royalty payments owed by us to Sanofi-Aventis. In June 2004, Novartis granted Vanda the worldwide rights to develop and commercialize iloperidone.

In October 2009, Vanda and Novartis amended and restated their sub-license agreement whereby Novartis acquired the U.S. and Canadian rights to commercialize Fanapt, the oral formulation of iloperidone approved in the U.S. Novartis also acquired the U.S. and Canadian development and commercialization rights to the depot formulation previously under development by Vanda and retained the right of first negotiation to co-market Fanapt and the depot formulation in the rest of the world. All of our rights and economic interests in iloperidone, including royalties on sales, remained essentially unchanged under these agreements.

In October 1995, we acquired from the Massachusetts Institute of Technology (“MIT”) an exclusive worldwide license to certain U.S. and foreign patents relating to our continuous drug delivery system. The exclusive nature of the MIT license is subject to our continued diligent product development activities. The agreement provides for the payment of a 2% royalty based on sales of products and processes incorporating the licensed technology, as well as 25% of other income (excluding research expense reimbursement) derived from sublicenses of the licensed technology.

In July 2005, we entered into an agreement with the University of Iowa Research Foundation. Under this agreement, we received an exclusive worldwide license to patent rights held by the University of Iowa Research Foundation covering the methods of treating biofilm formation, pseudomoras aeruginosa growth, human deficiency virus, and intracellular pathogens and pathogens causing chronic pulmonary infection using gallium maltolate. Under this agreement, we are required to pay a license issuance fee and certain minimum annual royalty payments. In addition, we are required to pay royalties based on net sales of products and processes incorporating the licensed technology.

Patents and Proprietary Rights

We are the exclusive licensee under the MIT license to two U.S. patents and their European counterparts relating to a long-term drug delivery system. One patent term expired in 2010 while the second patent term expires in 2014. These dates do not include possible term extensions. Four additional patent applications have been filed which incorporate the use of specific compounds with the continuous delivery technology, including two applications related to Probuphine for the potential treatment of opioid addiction and chronic pain. In June 2010, the United States Patent and Trademark Office (“USPTO”) issued a patent covering Probuphine for the treatment of opiate addiction. Titan is the assignee of this patent which claims a method for treating opiate addiction with a subcutaneously implanted device comprising buprenorphine and ethylene vinyl acetate, a

5

biocompatible copolymer that releases buprenorphine continuously for extended periods of time. This patent, which also includes certain additional claims covering the composition and dimensions of the device, will expire in April 2024. Patents have issued in Australia, India, Mexico and New Zealand. Further prosecution of these applications is currently proceeding at the USPTO and corresponding agencies in Europe, Canada, Japan, India and Hong Kong.

We hold a license from Sanofi-Aventis under certain issued U.S. patents and certain issued foreign patents relating to iloperidone and its methods of use in the treatment of psychiatric disorders, psychotic disorders and analgesia. The term of the U.S. patent that covers certain aspects of our iloperidone product expires in April 2017, inclusive of a six month extension possible for approval of pediatric indication. Limited foreign patent protection remains in Lichtenstein, Georgia, Korea and the Philippines.

We are the licensee from the University of Iowa Research Foundation (“UIRF”) of two issued U.S. patents (expiring in 2016) relating to methods of use of gallium compounds to inhibit the growth of P. aeruginosa, and the treatment of infections by pathogens causing chronic pulmonary infection. We are also the licensee from UIRF of certain rights to patent applications covering the use of gallium complexes in preventing and also treating bacterial biofilm-based infections, for which patents have issued in South Africa and Mexico and prosecution in the U.S., Canada, Europe, Australia, New Zealand and some Asian countries continues.

Competition

The pharmaceutical and biotechnology industries are characterized by rapidly evolving technology and intense competition. Many companies of all sizes, including major pharmaceutical companies and specialized biotechnology companies, are engaged in the development and commercialization of therapeutic agents designed for the treatment of the same diseases and disorders that we target. Many of our competitors have substantially greater financial and other resources, larger research and development staff and more experience in the regulatory approval process. Moreover, potential competitors have or may have patents or other rights that conflict with patents covering our technologies. For risks we face with respect to competition, see “Risk Factors—We face intense competition.”

With respect to Probuphine, Reckitt Benckiser Group, PLC, markets globally a sublingual buprenorphine product (tablet and film formulations) for the treatment of opioid dependence. This product (Subutex®, Suboxone®) which is administered daily, will compete with our six-month implantable product for treating opioid dependence. Other forms of buprenorphine are also in development by other companies, including intramuscular injections, buccal delivery and intranasally delivered buprenorphine, which also might compete with our product. In 2010, Alkermes, Inc. received FDA approval to market Vivitrol®, a one month depot injection of naltrexone as a maintenance treatment for opioid dependent patients who have successfully achieved abstinence. We are aware of one month depot formulations of buprenorphine in early clinical development for the treatment of opioid dependence, but we are not aware of any six-month formulations being developed other than Probuphine.

Manufacturing

The manufacturing of Probuphine has primarily been conducted at DPT Laboratories, Inc., and we are in the process of expanding the manufacturing facility at this contract manufacturer to establish commercial scale capability to support the potential market launch of Probuphine, and ongoing demand following potential approval by the FDA.

Government Regulation

In order to obtain FDA approval of a new drug, a company generally must submit proof of purity, potency, safety and efficacy, among other regulatory standards. In most cases, such proof entails extensive clinical and pre-clinical laboratory tests.

6

The procedure for obtaining FDA approval to market a new drug involves several steps. Initially, the manufacturer must conduct pre-clinical animal testing to demonstrate that the product does not pose an unreasonable risk to human subjects in clinical studies. Upon completion of such animal testing, an Investigational New Drug (“IND”) application must be filed with the FDA before clinical studies may begin. An IND application consists of, among other things, information about the proposed clinical trials. Among the conditions for clinical studies and IND approval is the requirement that the prospective manufacturer’s quality control and manufacturing procedures conform to current Good Manufacturing Practices (“cGMP”), which must be followed at all times. Once the IND is approved (or if the FDA does not respond within 30 days), the clinical trials may begin.

The results of the pre-clinical and clinical testing on new drugs, if successful, are submitted to the FDA in the form of a New Drug Application (“NDA”). The NDA approval process requires substantial time and effort and there can be no assurance that any approval will be granted on a timely basis, if at all. The FDA may refuse to approve an NDA if applicable regulatory requirements are not satisfied. Product approvals, if granted, may be withdrawn if compliance with regulatory standards is not maintained or problems occur following initial marketing.

The FDA may also require post-marketing testing and surveillance of approved products, or place other conditions on their approvals. These requirements could cause it to be more difficult or expensive to sell the products, and could therefore restrict the commercial applications of such products. Product approvals may be withdrawn if compliance with regulatory standards is not maintained or if problems occur following initial marketing. With respect to patented products or technologies, delays imposed by the governmental approval process may materially reduce the period during which we will have the exclusive right to exploit such technologies.

We believe we are in compliance with all material applicable regulatory requirements. However, see “Risk Factors—We must comply with extensive government regulations” for additional risks we face regarding regulatory requirements and compliance.

Foreign Regulatory Issues

Sales of pharmaceutical products outside the United States are subject to foreign regulatory requirements that vary widely from country to country. Whether or not FDA approval has been obtained, approval of a product by a comparable regulatory authority of a foreign country must generally be obtained prior to the commencement of marketing in that country. Although the time required to obtain such approval may be longer or shorter than that required for FDA approval, the requirements for FDA approval are among the most detailed in the world and FDA approval generally takes longer than foreign regulatory approvals.

Employees

At December 31, 2011, we had 12 full-time employees and several consultants.

7

| Item 1A. | Risk Factors |

We do not have the financial or other resources to complete the regulatory approval process or commercialize any product and may not be able to obtain the necessary financing and other resources.

At December 31, 2011, we had cash of approximately $5.4 million, which we believe is sufficient to fund our planned operations into the second quarter of 2012. We will require additional financing in order to complete preparation of the NDA and the regulatory process and seek approval to commercialize Probuphine, for which financing may not be available on acceptable terms, if at all. Furthermore, we do not have the financial or other resources necessary to commercialize any product and will need either to enter into a corporate partnership or licensing arrangement or raise the substantial funds required to establish our own sales, marketing and distribution capabilities in order to commercialize Probuphine (or any other product we may successfully develop) in the event regulatory approval is obtained. There can be no assurance that we will be able to enter into any such partnership or arrangement or raise such funds on acceptable terms, if at all.

We must comply with extensive government regulations.

The research, development, manufacture labeling, storage, record-keeping, advertising, promotion, import, export, marketing and distribution of pharmaceutical products are subject to an extensive regulatory approval process by the FDA in the U.S. and comparable health authorities in foreign markets. The process of obtaining required regulatory approvals for drugs is lengthy, expensive and uncertain. Approval policies or regulations may change and the FDA and foreign authorities have substantial discretion in the pharmaceutical approval process, including the ability to delay, limit or deny approval of a product candidate for many reasons. Despite the time and expense invested in clinical development of product candidates, regulatory approval is never guaranteed. Regulatory approval may entail limitations on the indicated usage of a drug, which may reduce the drug’s market potential. Even if regulatory clearance is obtained, post-market evaluation of the products, if required, could result in restrictions on a product’s marketing or withdrawal of the product from the market, as well as possible civil and criminal sanctions. Our business will be seriously harmed if our regulatory submissions are delayed or we cancel plans to make submissions for proposed products for any reason.

Probuphine may not receive FDA approval.

Probuphine, which has completed Phase 3 clinical development and is in the NDA preparation stage, will require significant further capital expenditures and regulatory clearances prior to commercialization. Even if we are able to obtain the requisite funding to complete the NDA submission and regulatory process, the FDA can delay, limit or deny approval of the product for many reasons, including:

| • | we may be unable to demonstrate to the satisfaction of the FDA that a product candidate is safe and effective for any indication; |

| • | the FDA may disagree with our interpretation of data from non-clinical studies or clinical trials; |

| • | we may be unable to demonstrate that the product’s clinical and other benefits outweigh any safety or other perceived risks; |

| • | the FDA may fail to approve the manufacturing processes or facilities of third-party manufacturers with which we, or our collaborators, contract; or |

| • | the approval policies or regulations of the FDA may significantly change in a manner rendering our clinical data insufficient for approval. |

Of the large number of drugs in development, only a small percentage successfully complete the FDA regulatory approval process and are commercialized. Any delay in obtaining, or inability to obtain, applicable FDA approval would prevent commercialization of Probuphine in the U.S. and would materially adversely impact our business and prospects.

8

If any product candidate that we successfully develop does not achieve broad market acceptance among physicians, patients, healthcare payors and the medical community, the revenues that it generates from their sales will be limited.

Even if Probuphine or any other product candidate receives regulatory approval, they may not gain market acceptance among physicians, patients, healthcare payors and the medical community. Coverage and reimbursement of our product candidates by third-party payors, including government payors, generally is also necessary for commercial success. The degree of market acceptance of any approved products will depend on a number of factors, including:

| • | the efficacy and safety as demonstrated in clinical trials; |

| • | the clinical indications for which the product is approved; |

| • | acceptance by physicians, operators of hospitals and clinics and patients of the product as a safe and effective product; |

| • | the potential and perceived advantages of the product over alternative treatments; |

| • | the safety of the product in broader patient groups, including its use outside of approved indications; |

| • | the cost of treatment in relation to alternative treatments; |

| • | the availability of adequate reimbursement and pricing by third parties and government authorities; |

| • | the prevalence and severity of adverse events; |

| • | the effectiveness of sales and marketing efforts; and |

| • | unfavorable publicity relating to the product. |

If any product candidate is approved but does not achieve an adequate level of acceptance by physicians, hospitals and clinics, healthcare payors and patients, we may not generate significant revenue from such products.

We must comply with extensive government regulations.

The development, manufacture, labeling, storage, record-keeping, advertising, promotion, import, export, marketing and distribution of pharmaceutical products are subject to an extensive regulatory approval process by the FDA in the U.S. and comparable health authorities in foreign markets. The process of obtaining required regulatory approvals for drugs is lengthy, expensive and uncertain. Approval policies or regulations may change and the FDA and foreign authorities have substantial discretion in the pharmaceutical approval process, including the ability to delay, limit or deny approval of a product candidate for many reasons. Despite the time and expense invested in clinical development of product candidates, regulatory approval is never guaranteed. Regulatory approval may entail limitations on the indicated usage of a drug, which may reduce the drug’s market potential. Even if regulatory clearance is obtained, post-market evaluation of the products, if required, could result in restrictions on a product’s marketing or withdrawal of the product from the market, as well as possible civil and criminal sanctions. Our business will be seriously harmed if our regulatory submissions are delayed or we cancel plans to make submissions for proposed products for any reason.

We face risks associated with third parties conducting preclinical studies and clinical trials of our products; as well as our dependence on third parties to manufacture any products that we may successfully develop.

We depend on third-party laboratories and medical institutions to conduct preclinical studies and clinical trials for our products and other third-party organizations to perform data collection and analysis, all of which must maintain both good laboratory and good clinical practices. We also depend upon third party manufacturers for the production of any products we may successfully develop to comply with current Good Manufacturing Practices of the FDA, which are similarly outside our direct control. If third party laboratories and medical institutions conducting studies of our products fail to maintain both good laboratory and clinical practices, the

9

studies could be delayed or have to be repeated. Similarly, if the manufacturers of any products we develop in the future fail to comply with current Good Manufacturing Practices of the FDA, we may be forced to cease manufacturing such product until we have found another third party to manufacture the product.

We face risks associated with product liability lawsuits that could be brought against us.

Our clinical liability insurance coverage may not be sufficient to cover claims that may be made against us in the event that the use or misuse of our product candidates causes, or merely appears to have caused, personal injury or death. Any claims against us, regardless of their merit, could severely harm our financial condition, strain our management and other resources or destroy the prospects for commercialization of the product which is the subject of any such claim.

We may be unable to protect our patents and proprietary rights.

Our future success will depend to a significant extent on our ability to:

| • | obtain and keep patent protection for our products and technologies on an international basis; |

| • | enforce our patents to prevent others from using our inventions; |

| • | maintain and prevent others from using our trade secrets; and |

| • | operate and commercialize products without infringing on the patents or proprietary rights of others. |

We cannot assure you that our patent rights will afford any competitive advantages, and these rights may be challenged or circumvented by third parties. Further, patents may not be issued on any of our pending patent applications in the U.S. or abroad. Because of the extensive time required for development, testing and regulatory review of a potential product, it is possible that before a potential product can be commercialized, any related patent may expire or remain in existence for only a short period following commercialization, reducing or eliminating any advantage of the patent. For example, the two U.S. patents licensed by Titan under the MIT license have already expired, and we must rely on the “method of use” patent application for Probuphine to get patent protection and market exclusivity. If we sue others for infringing our patents, a court may determine that such patents are invalid or unenforceable. Even if the validity of our patent rights is upheld by a court, a court may not prevent the alleged infringement of our patent rights on the grounds that such activity is not covered by our patent claims.

In addition, third parties may sue us for infringing their patents. In the event of a successful claim of infringement against us, we may be required to:

| • | pay substantial damages; |

| • | stop using our technologies and methods; |

| • | stop certain research and development efforts; |

| • | develop non-infringing products or methods; and |

| • | obtain one or more licenses from third parties. |

If required, we cannot assure you that we will be able to obtain such licenses on acceptable terms, or at all. If we are sued for infringement, we could encounter substantial delays in development, manufacture and commercialization of our product candidates. Any litigation, whether to enforce our patent rights or to defend against allegations that we infringe third party rights, will be costly, time consuming, and may distract management from other important tasks.

10

We also rely in our business on trade secrets, know-how and other proprietary information. We seek to protect this information, in part, through the use of confidentiality agreements with employees, consultants, advisors and others. Nonetheless, we cannot assure you that those agreements will provide adequate protection for our trade secrets, know-how or other proprietary information and prevent their unauthorized use or disclosure. To the extent that consultants, key employees or other third parties apply technological information independently developed by them or by others to our proposed products, disputes may arise as to the proprietary rights to such information, which may not be resolved in our favor.

We face intense competition.

Competition in the pharmaceutical and biotechnology industries is intense. We face, and will continue to face, competition from numerous companies that currently market, or are developing, products for the treatment of the diseases and disorders we have targeted. Many of these entities have significantly greater research and development capabilities, experience in obtaining regulatory approvals and manufacturing, marketing, financial and managerial resources than we have. We also compete with universities and other research institutions in the development of products, technologies and processes, as well as the recruitment of highly qualified personnel. Our competitors may succeed in developing technologies or products that are more effective than the ones we have under development or that render our proposed products or technologies noncompetitive or obsolete. In addition, our competitors may achieve product commercialization or patent protection earlier than we will.

Healthcare reform and restrictions on reimbursements may limit our financial returns.

Our ability or the ability of our collaborators to commercialize drug products, if any, may depend in part on the extent to which government health administration authorities, private health insurers and other organizations will reimburse consumers for the cost of these products. These third parties are increasingly challenging both the need for and the price of new drug products. Significant uncertainty exists as to the reimbursement status of newly approved therapeutics. Adequate third party reimbursement may not be available for our own or our collaborator’s drug products to enable us or them to maintain price levels sufficient to realize an appropriate return on their and our investments in research and product development.

We may not be able to retain our key management and scientific personnel.

As a company with a limited number of personnel, we are highly dependent on the services of our executive management and scientific staff, in particular Sunil Bhonsle and Marc Rubin, our President and Executive Chairman, respectively, and our Executive Vice President and Chief Development Officer, all of whom are parties to employment agreements with us. The loss of one or more of such individuals could substantially impair ongoing research and development programs and could hinder our ability to obtain corporate partners. Our success depends in large part upon our ability to attract and retain highly qualified personnel. We compete in our hiring efforts with other pharmaceutical and biotechnology companies, as well as universities and nonprofit research organizations, and we may not be successful in our efforts to attract and retain personnel.

Our stock price has been and will likely continue to be volatile.

Our stock price has experienced substantial fluctuations and could continue to fluctuate significantly due to a number of factors, including:

| • | variations in our anticipated or actual operating results or prospects; |

| • | sales of substantial amounts of our common stock; |

| • | announcements about us or about our competitors, including introductions of new products; |

| • | litigation and other developments relating to our patents or other proprietary rights or those of our competitors; |

11

| • | conditions in the pharmaceutical or biotechnology industries; |

| • | governmental regulation and legislation; and |

| • | change in securities analysts’ estimates of our performance, or our failure to meet analysts’ expectations. |

Our common stock is deemed to be a “penny stock,” which may make it more difficult for investors to sell their shares due to suitability requirements.

Our common stock is subject to Rule 15g-1 through 15g-9 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which imposes certain sales practice requirements on broker-dealers which sell our common stock to persons other than established customers and “accredited investors” (generally, individuals with a net worth in excess of $1,000,000 or annual incomes exceeding $200,000 (or $300,000 together with their spouses)). For transactions covered by this rule, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to the sale. This rule adversely affects the ability of broker-dealers to sell our common stock and the ability of our stockholders to sell their shares of common stock.

Additionally, our common stock is subject to the SEC regulations for “penny stock.” Penny stock includes any equity security that is not listed on a national exchange and has a market price of less than $5.00 per share, subject to certain exceptions. The regulations require that prior to any non-exempt buy/sell transaction in a penny stock, a disclosure schedule set forth by the SEC relating to the penny stock market must be delivered to the purchaser of such penny stock. This disclosure must include the amount of commissions payable to both the broker-dealer and the registered representative and current price quotations for the common stock. The regulations also require that monthly statements be sent to holders of penny stock that disclose recent price information for the penny stock and information of the limited market for penny stocks. These requirements adversely affect the market liquidity of our common stock.

Our net operating losses and research and development tax credits may not be available to reduce future federal and state income tax payments.

At December 31, 2011, we had federal net operating loss and tax credit carryforwards of $220.9 million and $7.6 million, respectively, and state net operating loss and tax credit carryforwards of $147.2 million and $7.4 million, respectively. Current federal and state tax laws include substantial restrictions on the utilization of net operating loss and tax credits in the event of an ownership change. We have performed a change of ownership analysis through December 31, 2011 and, accordingly, all of our net operating loss and tax credit carryforwards are available to offset future taxable income, if any.

Our stockholder rights plan may discourage or prevent a potential takeover, even if such a transaction would be beneficial to our stockholders.

In December 2011, our board of directors adopted a stockholder rights plan which provides for the potential issuance of dilutive junior preferred stock in the event of the acquisition or proposed acquisition of 15% or more of our outstanding common stock, which acquisition has not been approved by our board of directors.

While we believe that our stockholder rights plan enables our board of directors to maximize stockholder value, it may have the effect of delaying or preventing a change of control, even under circumstances that some stockholders may consider beneficial.

12

| Item 2. | Properties |

Our executive offices are located in approximately 9,255 square feet of office space in South San Francisco, California that we occupy under a three-year operating lease expiring in June 2013.

| Item 3. | Legal Proceedings |

We are currently not a party to any material legal or administrative proceedings and are not aware of any pending or threatened legal or administrative proceedings against us.

13

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

(a) Price Range of Securities

From December 2008 to June 2010, our common stock was quoted on the OTC Pink Sheets system maintained by Pink OTC Markets Inc. under the symbol TTNP.PK. The Pink Sheets market is extremely limited and any prices quoted may not have been a reliable indication of the value of our common stock. Since June 2, 2010, our common stock has been quoted on the OTC Bulletin Board under the symbol TTNP.OB.

The following table sets forth, for the periods indicated, the high and low sales prices per share of our common stock as reported by the Pink OTC Markets Inc. and OTC Bulletin Board, as applicable. The quotations reflect inter-dealer prices without retail markups, markdowns, or commissions and may not represent actual transactions. For current price information, stockholders are urged to consult publicly available sources.

| High | Low | |||||||

| Fiscal 2011 |

||||||||

| Fourth Quarter |

$ | 1.78 | $ | 1.06 | ||||

| Third Quarter |

$ | 2.08 | $ | 1.30 | ||||

| Second Quarter |

$ | 2.22 | $ | 1.30 | ||||

| First Quarter |

$ | 1.81 | $ | 1.17 | ||||

| Fiscal 2010 |

||||||||

| Fourth Quarter |

$ | 1.49 | $ | 0.99 | ||||

| Third Quarter |

$ | 1.20 | $ | 0.87 | ||||

| Second Quarter |

$ | 1.86 | $ | 0.92 | ||||

| First Quarter |

$ | 2.49 | $ | 1.70 | ||||

(b) Approximate Number of Equity Security Holders

As of March 9, 2012, there were approximately 142 record holders of our common stock.

(c) Dividends

We have never paid a cash dividend on our common stock and anticipate that for the foreseeable future any earnings will be retained for use in our business and, accordingly, do not anticipate the payment of cash dividends.

14

Performance Graph

The information contained in the Performance Graph shall not be deemed to be “soliciting material” or “filed” with the SEC or subject to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), except to the extent that we specifically incorporate it by reference into a document filed under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act.

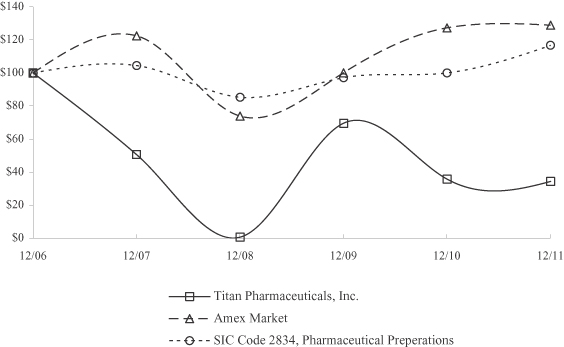

The following graph compares the cumulative total stockholder return on our common stock with the cumulative total stockholder return of (i) the AMEX Market Index, and (ii) a peer group index consisting of companies reporting under the Standard Industrial Classification Code 2834 (Pharmaceutical Preparations). The graph assumes $100 invested on December 31, 2006 and assumes dividends reinvested. Measurement points are at the last trading day of the fiscal years ended December 31, 2007, 2008, 2009, 2010 and 2011. The stock price performance on the following graph is not necessarily indicative of future stock price performance.

COMPARE CUMULATIVE TOTAL RETURN

AMONG TITAN PHARMACEUTICALS, INC., AMEX MARKET INDEX AND

SIC CODE INDEX

15

| Item 6. | Selected Financial Data. |

The selected financial data presented below summarizes certain financial data which has been derived from and should be read in conjunction with our consolidated financial statements and notes thereto included in the section beginning on page F-1. See also “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Years Ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Total revenue |

$ | 4,068 | $ | 10,093 | $ | 79 | $ | 73 | $ | 24 | ||||||||||

| Operating expenses: |

||||||||||||||||||||

| Research and development |

11,206 | 12,855 | 2,456 | 16,235 | 12,244 | |||||||||||||||

| General and administrative |

3,368 | 3,263 | 3,438 | 9,756 | 6,213 | |||||||||||||||

| Other income (expense), net |

(4,697 | ) | (809 | ) | (71 | ) | 484 | 786 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss |

(15,203 | ) | (6,834 | ) | (5,886 | ) | (25,434 | ) | (17,647 | ) | ||||||||||

| Gain on retirement of preferred stock upon dissolution of subsidiary |

— | 1,241 | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss applicable to common stockholders |

$ | (15,203 | ) | $ | (5,593 | ) | $ | (5,886 | ) | $ | (25,434 | ) | $ | (17,647 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic and diluted net loss per common share |

$ | (0.26 | ) | $ | (0.09 | ) | $ | (0.10 | ) | $ | (0.44 | ) | $ | (0.41 | ) | |||||

| Shares used in computing: |

||||||||||||||||||||

| Basic and diluted net loss per common share |

59,324 | 59,248 | 58,473 | 58,285 | 42,998 | |||||||||||||||

| As of December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash |

$ | 5,406 | $ | 3,180 | $ | 3,300 | $ | 4,672 | $ | 30,016 | ||||||||||

| Working capital |

4,839 | (706 | ) | 2,069 | 2,759 | 26,200 | ||||||||||||||

| Total assets |

10,217 | 4,752 | 3,726 | 5,668 | 30,844 | |||||||||||||||

| Total stockholders’ (deficit) equity |

(20,079 | ) | (6,053 | ) | (1,448 | ) | 1,793 | 25,347 | ||||||||||||

16

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Forward-Looking Statements

Statements in the following discussion and throughout this report that are not historical in nature are “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. You can identify forward-looking statements by the use of words such as “expect,” “anticipate,” “estimate,” “may,” “will,” “should,” “intend,” “believe,” and similar expressions. Although we believe the expectations reflected in these forward-looking statements are reasonable, such statements are inherently subject to risk and we can give no assurances that our expectations will prove to be correct. Actual results could differ from those described in this report because of numerous factors, many of which are beyond our control. These factors include, without limitation, those described under Item 1A “Risk Factors.” We undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this report or to reflect actual outcomes. Please see “Note Regarding Forward-Looking Statements” at the beginning of this Annual Report on Form 10-K.

The following discussion of our financial condition and results of operations should be read in conjunction with our consolidated financial statements and the related notes thereto and other financial information appearing elsewhere in this Annual Report on Form 10-K.

Overview

Our principal asset is Probuphine™, the first slow release implant formulation of buprenorphine, designed to maintain a stable, round the clock blood level of the medicine in patients for six months following a single treatment. Daily treatment of opioid dependence with sublingual buprenorphine formulations is over a $1 billion market in the U.S., and a transdermal formulation of buprenorphine for the treatment of chronic pain entered the U.S. market in 2011. Probuphine is being developed for the treatment of opioid dependence with the potential to enhance patient compliance to medication, and limit diversion and accidental use of the daily dosed formulations. In October 2011, we had a Pre-New Drug Application meeting with the U.S. Food and Drug Administration (the “FDA”) that provided clear guidance on the requirements for submitting a New Drug Application (“NDA”). The clinical development program is now complete and preparation of the NDA is in process. At the request of the FDA, we are conducting additional analytical testing of the ethylene vinyl acetate (an inactive co-polymer in Probuphine) and the final product, Probuphine, in order to complete full characterization and establish ‘in-use’ stability. We have also commenced a program with our contract manufacturer to scale-up the manufacturing process for commercial production. We expect to complete these steps and be in a position to submit the NDA in the third quarter of 2012. Our goal is to enter into one or more partnerships with capable pharmaceutical companies to commercialize Probuphine in the U.S. and foreign markets, as well as to potentially develop the product for the treatment of chronic pain.

Probuphine is the first product to utilize ProNeura™, our novel, proprietary, long-term drug delivery technology. Our ProNeura technology has the potential to be used in developing products for the treatment of other chronic conditions, such as Parkinson’s disease, where maintaining stable, round the clock blood levels of a drug can benefit the patient and improve medical outcomes.

Under a sublicense agreement with Novartis Pharma AG (“Novartis”), we are entitled to royalty revenue of 8-10% of net sales of Fanapt® (iloperidone), an atypical antipsychotic compound being marketed in the U.S. by Novartis for the treatment of schizophrenia, based on a licensed U.S. patent that expires in April 2017 (inclusive of a six month pediatric extension). During 2011, we entered into several agreements with Deerfield Management (“Deerfield”), a healthcare investment fund, in which we agreed to pay most of this future royalty stream to Deerfield and have been using the proceeds to advance the development of Probuphine and for general corporate purposes. We have retained a portion of the royalty revenue from net sales of Fanapt in excess of specified annual threshold levels; however, based on sales levels to date, it is unlikely that we will receive any revenue from Fanapt in the next several years, if ever.

17

Critical Accounting Policies and the Use of Estimates

The preparation of our financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported in our consolidated financial statements and accompanying notes. Actual results could differ materially from those estimates. We believe the following accounting policies for the years ended December 31, 2011 and 2010 to be applicable:

Revenue Recognition

We generate revenue principally from royalty payments, collaborative research and development arrangements, technology licenses, and government grants. Consideration received for revenue arrangements with multiple components is allocated among the separate units of accounting based on their respective selling prices. The selling price for each unit is based on vendor-specific objective evidence, or VSOE, if available, third party evidence if VSOE is not available, or estimated selling price if neither VSOE nor third party evidence is available. The applicable revenue recognition criteria are then applied to each of the units.

Revenue is recognized when the four basic criteria of revenue recognition are met: (1) a contractual agreement exists; (2) transfer of technology has been completed or services have been rendered; (3) the fee is fixed or determinable; and (4) collectibility is reasonably assured. For each source of revenue, we comply with the above revenue recognition criteria in the following manner:

| • | Royalties earned are based on third-party sales of licensed products and are recorded in accordance with contract terms when third-party results are reliably measurable and collectibility is reasonably assured. Pursuant to certain license agreements, we earn royalties on the sale of Fanapt™ by Novartis Pharma AG in the U.S. As described in Note 8, Royalty Liability, we are obligated to pay royalties on such sales to Sanofi-Aventis and Deerfield. As we have no performance obligations under the license agreements, we have recorded the royalties earned, net of royalties we are obligated to pay, as revenue in our Consolidated Statement of Operations. |

| • | Collaborative arrangements typically consist of non-refundable and/or exclusive technology access fees, cost reimbursements for specific research and development spending, and various milestone and future product royalty payments. If the delivered technology does not have stand-alone value or if we do not have objective or reliable evidence of the fair value of the undelivered component, the amount of revenue allocable to the delivered technology is deferred. Non-refundable upfront fees with stand-alone value that are not dependent on future performance under these agreements are recognized as revenue when received, and are deferred if we have continuing performance obligations and have no evidence of fair value of those obligations. Cost reimbursements for research and development spending are recognized when the related costs are incurred and when collections are reasonably expected. Payments received related to substantive, performance-based “at-risk” milestones are recognized as revenue upon achievement of the clinical success or regulatory event specified in the underlying contracts, which represent the culmination of the earnings process. Amounts received in advance are recorded as deferred revenue until the technology is transferred, costs are incurred, or a milestone is reached. |

| • | Technology license agreements typically consist of non-refundable upfront license fees, annual minimum access fees or royalty payments. Non-refundable upfront license fees and annual minimum payments received with separable stand-alone values are recognized when the technology is transferred or accessed, provided that the technology transferred or accessed is not dependent on the outcome of our continuing research and development efforts. |

| • | Government grants, which support our research efforts in specific projects, generally provide for reimbursement of approved costs as defined in the notices of grants. Grant revenue is recognized when associated project costs are incurred. |

18

Share-Based Payments

We recognize compensation expense for all share-based awards made to employees and directors. The fair value of share-based awards is estimated at the grant date based on the fair value of the award and is recognized as expense, net of estimated pre-vesting forfeitures, ratably over the vesting period of the award. We use the Black-Scholes option pricing model to estimate the fair value method of our awards. Calculating stock-based compensation expense requires the input of highly subjective assumptions, including the expected term of the share-based awards, stock price volatility, and pre-vesting forfeitures. We estimate the expected term of stock options granted for the years ended December 31, 2011, 2010 and 2009 based on the historical experience of similar awards, giving consideration to the contractual terms of the share-based awards, vesting schedules and the expectations of future employee behavior. We estimate the volatility of our common stock at the date of grant based on the historical volatility of our common stock. The assumptions used in calculating the fair value of stock-based awards represent our best estimates, but these estimates involve inherent uncertainties and the application of management judgment. As a result, if factors change and we use different assumptions, our stock-based compensation expense could be materially different in the future. In addition, we are required to estimate the expected pre-vesting forfeiture rate and only recognize expense for those shares expected to vest. We estimate the pre-vesting forfeiture rate based on historical experience. If our actual forfeiture rate is materially different from our estimate, our stock-based compensation expense could be significantly different from what we have recorded in the current period.

Income Taxes

We make certain estimates and judgments in determining income tax expense for financial statement purposes. These estimates and judgments occur in the calculation of certain tax assets and liabilities, which arise from differences in the timing of recognition of revenue and expense for tax and financial statement purposes.

As part of the process of preparing our consolidated financial statements, we are required to estimate our income taxes in each of the jurisdictions in which we operate. This process involves us estimating our current tax exposure under the most recent tax laws and assessing temporary differences resulting from differing treatment of items for tax and accounting purposes.

We assess the likelihood that we will be able to recover our deferred tax assets. We consider all available evidence, both positive and negative, expectations and risks associated with estimates of future taxable income and ongoing prudent and feasible tax planning strategies in assessing the need for a valuation allowance. If it is not more likely than not that we will recover our deferred tax assets, we will increase our provision for taxes by recording a valuation allowance against the deferred tax assets that we estimate will not ultimately be recoverable.

Clinical Trial Accrual

We also record accruals for estimated ongoing clinical trial costs. Clinical trial costs represent costs incurred by clinical research organizations, (“CROs”), and clinical sites. These costs are recorded as a component of research and development expenses. Under our agreements, progress payments are typically made to investigators, clinical sites and CROs. We analyze the progress of the clinical trials, including levels of patient enrollment, invoices received and contracted costs when evaluating the adequacy of accrued liabilities. Significant judgments and estimates must be made and used in determining the accrued balance in any accounting period. Actual results could differ from those estimates under different assumptions. Revisions are charged to expense in the period in which the facts that give rise to the revision become known. The actual clinical trial costs for the Probuphine studies conducted in the past three years have not differed materially from the estimated projection of expenses.

19

Warrants Issued in Connection with Equity Financing

We generally account for warrants issued in connection with equity financings as a component of equity, unless there is a deemed possibility that we may have to settle warrants in cash. For warrants issued with deemed possibility of cash settlement, we record the fair value of the issued warrants as a liability at each reporting period and record changes in the estimated fair value as a non-cash gain or loss in the Condensed Consolidated Statements of Operations.

Liquidity and Capital Resources

| 2011 | 2010 | 2009 | ||||||||||

| (in thousands) | ||||||||||||

| As of December 31: |

||||||||||||

| Cash |

$ | 5,406 | $ | 3,180 | $ | 3,300 | ||||||

| Working capital |

$ | 4,839 | $ | (706 | ) | $ | 2,069 | |||||

| Current ratio |

1.9:1 | 0.9:1 | 2.3:1 | |||||||||

| Years Ended December 31: |

||||||||||||

| Cash used in operating activities |

$ | (14,476 | ) | $ | (4,657 | ) | $ | (5,407 | ) | |||

| Cash (used in) provided by investing activities |

$ | (234 | ) | $ | (28 | ) | $ | 2 | ||||

| Cash provided by financing activities |

$ | 16,936 | $ | 4,565 | $ | 4,033 | ||||||

We have funded our operations since inception primarily through sales of our securities, as well as with proceeds from warrant and option exercises, corporate licensing and collaborative agreements, and government-sponsored research. At December 31, 2011, we had approximately $5.4 million of cash compared to approximately $3.2 million at December 31, 2010.

Our operating activities used approximately $14.5 million during the year ended December 31, 2011. This consisted primarily of the net loss for the period of approximately $15.2 million, approximately $1.9 million related to net non-cash gains on changes in the fair value of warrants and approximately $1.4 million related to net changes in operating assets and liabilities. This was offset in part by approximately $2.8 million related to the non-cash interest expense on our long-term debt and royalty liability, non-cash charges of approximately $32,000 related to depreciation, and approximately $1.2 million related to stock-based compensation expenses. Uses of cash in operating activities were primarily to fund product development programs and administrative expenses. The license agreements with Sanofi-Aventis and MIT require us to pay royalties on future product sales. In addition, in order to maintain license and other rights while products are under development, we must comply with customary licensee obligations, including the payment of patent-related costs, annual minimum license fees, meeting project-funding milestones and diligent efforts in product development. The aggregate commitments we have under these agreements, including minimum license payments, for the next 12 months is approximately $34,000. See “Item 1. Business—License Agreements.”

Net cash used in investing activities of approximately $234,000 during the year ended December 31, 2011 consisted of approximately $236,000 related to purchases of equipment, which was offset in part by approximately $2,000 related to disposals of equipment.

Net cash provided by financing activities of approximately $16.9 million during the year ended December 31, 2011 consisted of approximately $16.5 million of net proceeds from the Deerfield transaction described below and proceeds of approximately $8.0 million received in exchange for substantially all of the remaining Fanapt royalties as described below. This was offset by payments of approximately $7.6 million to repay our outstanding indebtedness to Oxford.

On March 15, 2011, we entered into several agreements with entities affiliated with Deerfield pursuant to which Deerfield agreed to provide $20.0 million in funding to us. Funding occurred on April 5, 2011. Pursuant to

20

the terms of a facility agreement, we issued Deerfield promissory notes in the aggregate principal amount of $20.0 million. The long-term debt bears interest at 8.5% per annum, payable quarterly, and the long-term debt is repayable over five years, with 10% of the principal amount due on the first anniversary, 15% due on the second anniversary, and 25% due on each of the next three anniversaries. We paid Deerfield a facility fee of $0.5 million. The long-term debt is secured by our assets and has a provision for pre-payment. Deerfield has the right to have the long-term debt repaid at 110% of the principal amount in the event we complete a major transaction, which includes, but is not limited to, a merger or sale of our company or the sale of Fanapt or Probuphine. Under a royalty agreement, in exchange for $3.0 million that was recorded as royalty liability, we agreed to pay Deerfield 2.5% of the aggregate royalties on net sales of Fanapt, subsequent to the funding date, constituting a portion of the royalty revenue we receive from Novartis. The agreements with Deerfield also provide us with the option to repurchase the royalty rights for $40.0 million.

On April 5, 2011, we used approximately $7.6 million of proceeds from the Deerfield funding to repay Oxford in full, including required final payments aggregating $480,000.

On November 14, 2011, we entered into several agreements with Deerfield pursuant to which we agreed to provide a substantial portion of the remaining future royalties on the sales of Fanapt in exchange for $5.0 million in cash that was recorded as royalty liability, a $10.0 million reduction in the principal amount owed to Deerfield under the existing facility agreement and a revised principal repayment schedule of $2.5 million per year for four years commencing in April 2013 to retire the remaining long-term debt of $10.0 million. Deerfield is entitled to the balance of our portion of the royalties on Fanapt (5.5% to 7.5% of net sales, net of the 2.5% we previously agreed to pay to Deerfield) up to specified threshold levels of net sales of Fanapt and 40% of the royalties above the threshold level. We retain 60% of the royalties on net sales of Fanapt above the threshold levels, subject to an agreement that half of any such retained royalties will go towards repayment of our outstanding debt to Deerfield. Funding of the transaction took place on November 25, 2011.

We expect to continue to incur substantial additional operating losses from costs related to the continuation of research and development, clinical trials, the regulatory process, and administrative activities. We believe that our working capital at December 31, 2011, which includes the proceeds from the recent Deerfield transactions, is sufficient to fund our planned operations late into the second quarter of 2012, including the preparation of the Probuphine NDA. In the event we are unable to enter into a corporate partnership or licensing arrangement during this period that provides us with the funds required to complete the regulatory process and commercialize Probuphine, if approved, we will need to obtain additional financing, either through the sale of debt or equity securities, to continue our Probuphine program and other product development activities. If we are unable to complete a debt or equity offering, or otherwise obtain sufficient financing when and if needed, we may be required to reduce, defer or discontinue one or more of our product development activities.

The following table sets forth the aggregate contractual cash obligations as of December 31, 2011 (in thousands):

| Payments Due by Period | ||||||||||||||||||||

| Contractual obligations |

Total | < 1 year | 1-3 years | 3-5 years | 5 years+ | |||||||||||||||

| Operating leases |

$ | 342 | $ | 221 | $ | 121 | $ | — | $ | — | ||||||||||

| License agreements |

170 | 34 | 68 | 68 | — | |||||||||||||||

| Debt obligation(1) |

12,338 | 850 | 6,169 | 5,319 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total contractual cash obligations |

$ | 12,850 | $ | 1,105 | $ | 6,358 | $ | 5,387 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

For a full discussion of risks and uncertainties regarding our need for additional financing, see “Risk Factors—We do not have the financial or other resources to complete the regulatory approval process or commercialize any product and may not be able to obtain the necessary financing and other resources.”

| (1) | Excludes payments related to the royalty liability with Deerfield under the March 2011 and November 2011 Royalty Agreements. |

21

Results of Operations

Year Ended December 31, 2011 Compared to Year Ended December 31, 2010

Our net loss applicable to common stockholders for 2011 was approximately $15.2 million, or approximately $0.26 per share, compared to our net loss applicable to common stockholders of approximately $5.6 million, or approximately $0.09 per share, for 2010. Our net loss for 2011 includes a non-cash gain of $1.9 million resulting from changes in the fair value of warrants issued as part of the March 2011 Deerfield transaction.

We generated royalty revenues during 2011 of approximately $3.6 million compared to approximately $2.5 million during 2010. We generated grant revenues during 2011 of approximately $0.5 million compared to approximately $7.6 million during 2010. We generated no revenues from licensing agreements in 2011 compared to approximately $24,000 during 2010. Royalty revenues during 2011 and 2010 consisted of royalties on sales of Fanapt. Grant revenues during 2011 and 2010 consisted of proceeds from the NIH grants related to our Probuphine and ProNeura related programs.

Research and development expenses for 2011 were approximately $11.2 million compared to approximately $12.9 million in 2010, a decrease of approximately $1.7 million, or 13%. The decrease in research and development costs was primarily associated with a decrease in external research and development expenses related to the Phase 3 clinical trials of our Probuphine product which were completed in 2011. External research and development expenses include direct expenses such as clinical research organization charges, investigator and review board fees, patient expense reimbursements and contract manufacturing expenses. During 2011, our external research and development expenses relating to our Probuphine product development program were approximately $7.7 million compared to approximately $10.1 million for 2010. Other research and development expenses include internal operating costs such as clinical research and development personnel-related expenses, clinical trials-related travel expenses, and allocation of facility and corporate costs. As a result of the risks and uncertainties inherently associated with pharmaceutical research and development activities described elsewhere in this report, we are unable to estimate the specific timing and future costs of our clinical development programs or the timing of material cash inflows, if any, from our products or product candidates.

General and administrative expenses for 2011 were approximately $3.4 million, compared to approximately $3.3 million in 2010, an increase of approximately $0.1 million, or 3%. The increase in general and administrative expenses was primarily related to increases in non-cash stock compensation costs of approximately $0.3 million, employee-related costs of approximately $0.3 million, marketing-related costs of approximately $0.2 million . This was offset in part by decreases in legal fees of approximately $0.3 million, consulting and professional fees of approximately $0.3 million, and facilities-related costs of $0.1 million.

Net other expense for 2011 was approximately $4.7 million, compared to approximately $0.8 million in 2010. The increase in net other expense during 2011 was primarily related to interest expense of approximately $6.2 million on the Deerfield long-term debt and $0.2 million of interest expense related to the Oxford loans. This was offset in part by a $1.9 million non-cash gain related to decreases in the fair value of the Deerfield warrants.

Year Ended December 31, 2010 Compared to Year Ended December 31, 2009